Are you drowning in mounting bills, endless creditor calls, and financial uncertainty? If you’re seeking a way to break free from the stress and regain control of your finances, bankruptcy and debt consolidation are two options to explore. However, not all debt relief solutions are equal.

Bankruptcy provides a legal pathway to eliminate or restructure your debt, offering immediate relief and a fresh financial start. On the other hand, debt consolidation only simplifies payments into one, often leaving the underlying debt untouched and your financial challenges unresolved.

Suppose you’re tired of being chased by credit card companies, mortgage lenders, or payday loan providers. In that case, it’s important to understand why bankruptcy often provides a faster, more effective, and lasting solution. In this guide, we’ll break down the differences, weigh the pros and cons, and explain why bankruptcy may be the key to achieving genuine financial freedom. With the help of an experienced attorney, you can learn how an experienced attorney can help you make an informed decision that empowers you to control your financial future.

How Does Bankruptcy Work?

When you’re overwhelmed by mounting bills and creditors are calling nonstop, personal bankruptcy offers a lifeline, providing immediate relief and a path to rebuild your financial future. Governed by federal law, bankruptcy is a legal process designed to help individuals eliminate or restructure debt based on their unique circumstances.

Two Common Types of Consumer Bankruptcy

Chapter 7 Bankruptcy: Quick Debt Relief

- Purpose: Known as “liquidation bankruptcy,” Chapter 7 eliminates most unsecured debts, such as credit cards, medical bills, and personal loans, typically within 4-6 months.

- Advantages:

- Completely erases eligible debts, offering a true fresh start.

- It stops creditor harassment, lawsuits, and wage garnishments through automatic stay.

- Louisiana’s generous exemption laws allow most filers to retain essential assets such as a home, car, or retirement accounts.

Chapter 13 Bankruptcy: Asset Protection and Debt Reorganization

- Purpose: Often called “reorganization bankruptcy,” Chapter 13 enables individuals with a regular income to catch up on debts through an affordable 3-5-year repayment plan while keeping their assets.

- Advantages:

- Protects critical assets like your home and car from foreclosure or repossession.

- It stops creditors’ actions and provides breathing room for rebuilding your finances.

- No upfront attorney fees; costs are included in the repayment plan.

- Customizable plans based on your disposable income and financial situation.

Why Bankruptcy Is a Better Solution

Unlike debt consolidation, which combines payments and may leave you vulnerable to lawsuits or collection actions, bankruptcy is the superior debt relief option. It offers immediate and comprehensive protections that debt consolidation cannot match.

- Stops Creditor Actions Immediately: Bankruptcy invokes the automatic stay, a powerful legal shield that halts lawsuits, wage garnishments, foreclosures, and relentless collection calls from creditors. Debt consolidation does not provide such protection.

- Eliminates Debt, Doesn’t Just Rearrange It: Chapter 7 bankruptcy completely erases most unsecured debts, like credit cards and medical bills, while Chapter 13 lets you repay what you can afford over time. In contrast, debt consolidation merely consolidates payments, often leaving the full debt amount—and financial stress—intact.

- Protects Your Assets: Bankruptcy exemptions safeguard essential property, such as your home, car, and retirement accounts, ensuring you retain what matters most. Debt consolidation offers no such guarantees.

- Provides a Fresh Start: Bankruptcy is a legal tool designed to help you regain financial stability and rebuild your life. Debt consolidation often prolongs the debt cycle, keeping you trapped in financial uncertainty.”

Bankruptcy isn’t a sign of failure—it’s a tool to control your finances and move forward. The right legal guidance can be the decisive step toward lasting financial freedom and peace of mind.

Why Choose Chapter 7 Bankruptcy?

Imagine erasing your debts and stopping creditor harassment today—Chapter 7 bankruptcy makes this possible. Unlike debt consolidation, which merely combines payments and often fails to reduce the total debt, Chapter 7 eliminates most unsecured debts, such as credit cards, medical bills, and personal loans.

- Eliminates Most Debts: Chapter 7 provides a clean slate by discharging qualifying unsecured debts entirely.

- No Asset Surrender for Many Filers: While non-exempt property may be sold to repay creditors, many cases do not involve asset liquidation, thanks to generous exemption laws.

- Immediate Relief Through the Automatic Stay: As soon as you file, creditor harassment stops. No more collection calls, threatening letters, or wage garnishments—you gain the breathing room needed to rebuild your financial future.

For those drowning in unmanageable payments and mounting stress, Chapter 7 bankruptcy offers an efficient, straightforward path to financial freedom in as little as 4-6 months. With the right legal guidance, it’s the ultimate fresh start.

Why Choose Chapter 13 Bankruptcy?

What if you could catch up on overdue payments, protect your assets, and stop creditor actions like foreclosure? Chapter 13 bankruptcy is designed to help you do exactly that.

Unlike Chapter 7, which eliminates debts but may involve selling assets, Chapter 13 allows you to keep everything you’ve worked hard for while restructuring your debt into a manageable repayment plan over three to five years.

- Asset Protection: Chapter 13 helps you safeguard essential assets, such as your home and car, from foreclosure or repossession.

- Affordable Repayment Plans: Payments are tailored to your disposable income, covering only what you can reasonably afford after meeting your basic needs.

- Stops Creditor Actions: Foreclosures, repossessions, and collection lawsuits are halted immediately, giving you peace of mind and control.

- No Upfront Attorney Fees: Your repayment plan includes attorney fees, making Chapter 13 an accessible option for wage earners.

If you have a steady income but need time and structure to get back on track, Chapter 13 bankruptcy empowers you to catch up on debts, protect your property, and rebuild your financial stability. It’s not starting over—it’s reclaiming control.

How Does Debt Consolidation Work?

Debt consolidation attempts to simplify financial obligations by combining multiple debts, such as credit card balances, medical bills, and car loans, into one payment. However, it often fails to address the root causes of financial distress: the overwhelming debt itself and relentless creditor actions. Debt consolidation companies negotiate with creditors to create this arrangement.

However, the key word here is “attempt.” Debt consolidation only works if all creditors agree to the terms—and that’s often not the case. If even one creditor refuses, they can still pursue lawsuits, garnishments, or collection efforts against you, leaving you vulnerable.

The Drawbacks of Debt Consolidation

Debt consolidation programs frequently fail to deliver the comprehensive relief clients seek. Here’s why:

- No Guaranteed Creditor Cooperation: Creditors are not legally obligated to agree to a consolidation plan. If one or more creditors decline, they may still take legal action against you.

- No Legal Protection: Unlike bankruptcy, debt consolidation does not offer an automatic stay to halt creditor actions such as lawsuits, wage garnishments, or collection calls.

- Doesn’t Eliminate Debt: Consolidation reorganizes payments but does not reduce the overall debt amount. Interest and fees may still accumulate, prolonging financial struggles.

- High Costs with Minimal Support: Debt consolidation companies often charge excessive fees but provide little to no assistance if creditors sue or continue collection efforts. Many companies disclaim responsibility, saying, “We’re not lawyers.”

- Credit Damage: Missed or partial payments during the consolidation process can harm your credit score. Additionally, failure to address all creditors can result in ongoing financial distress.

Real-World Challenges of Debt Consolidation

At Simon Fitzgerald LLC, we’ve encountered countless clients who initially turned to debt consolidation programs, only to discover these programs worsened their financial struggles:

- Incomplete Debt Coverage: Many programs fail to include all creditors, leaving participants exposed to lawsuits and continued harassment.

- Overpromised, Underdelivered Results: Clients are often misled into believing consolidation is a cure-all, only to face mounting fees and little actual debt relief.

- Delayed Bankruptcy Filing: By discouraging bankruptcy as a ‘last resort,’ these programs delay the effective relief bankruptcy provides, prolonging financial hardship and increasing stress.

Why Bankruptcy Outperforms Debt Consolidation

Bankruptcy provides immediate and comprehensive relief that debt consolidation cannot match. Consider the key differences:

| Feature | Bankruptcy | Debt Consolidation |

| Debt Elimination | Chapter 7 erases unsecured debts. | Combines payments without reducing debt. |

| Upfront Costs | Chapter 13 requires no attorney fees upfront and often costs less in the long run. | Often, it involves high service fees and incomplete solutions. |

| Creditor Harassment | Stops immediately with the automatic stay. | Creditors can still pursue legal action. |

| Lawsuit Protection | Prevents lawsuits and garnishments. | Offers no legal protections. |

| Credit Recovery | Allows rebuilding within 12-24 months. | Credit may worsen if not managed properly. |

| Asset Protection | Protects homes, cars, and retirement accounts. | Does not safeguard assets. |

| Timeframe | Chapter 7: 4-6 months; Chapter 13: 3-5 years. | Varies, often years with little progress. |

Recognizing Debt Relief Scams

Debt relief programs, such as debt consolidation and debt settlement, often target individuals in financial distress with promises of quick fixes. However, these programs frequently rely on deceptive practices, leaving participants in a worse financial situation. Here’s how to spot the warning signs of a scam and why bankruptcy often provides a safer, more effective solution.

The Reality of Debt Settlement

Debt settlement involves negotiating with creditors to reduce the amount owed, but it comes with significant risks:

- Creditors Are Not Obligated to Negotiate: The creditors may refuse to settle, leaving you liable for the full amount.

- Continued Financial Pressure: While negotiations take place, interest and late fees often accumulate, increasing your debt burden.

- Legal Vulnerability: Even if some debts are settled, creditors not included in the agreement can still sue you or pursue collection actions.

The Drawbacks of Debt Consolidation

Debt consolidation combines multiple debts into a single monthly payment, but it has serious limitations:

- No Debt Reduction: Consolidation reorganizes payments but does not reduce the total debt owed.

- Incomplete Protection: Creditors not included in the plan can continue to take legal action against you.

- High Fees and Limited Support: Many consolidation companies charge excessive fees and disclaim responsibility for lawsuits or collection actions.

- Prolonged Debt Cycle: Consolidated debt often grows due to interest and fees, prolonging financial struggles.

Red Flags of Debt Relief Scams

When evaluating debt relief programs, watch for these common warning signs:

- Demands for Upfront Payments

- It’s illegal for companies to require payment before services are rendered. Be cautious of any company asking for money upfront.

- Guaranteed Results

- No company can promise debt forgiveness or reduced payments. Only creditors have the authority to agree to these terms.

- Advising You to Stop Paying Creditors

- Stopping payments without a clear plan can result in lawsuits, late fees, and additional financial strain.

- Lack of Transparency

- Companies that avoid providing clear terms, fees, or an explanation of their process are often untrustworthy.

- Unsolicited Contact

- Be wary of aggressive, unsolicited phone calls, emails, or letters from debt relief agents.

- Pushy or Aggressive Behavior

- Legitimate companies respect your decision-making process. High-pressure tactics are a red flag.

Why Bankruptcy Outperforms Debt Relief Programs

Unlike debt settlement and consolidation, bankruptcy offers legal protections and comprehensive debt resolution:

- Stops Creditor Actions: Bankruptcy includes an automatic stay that immediately halts lawsuits, wage garnishments, and collection calls.

- Eliminates or Restructures Debt: Chapter 7 wipes out most unsecured debts, while Chapter 13 provides a structured repayment plan.

- Legal Oversight: Bankruptcy is a federally governed process, ensuring fairness and transparency.

- Asset Protection: Bankruptcy laws protect essential assets like your home, car, and retirement accounts.

- Cost-Effectiveness: Bankruptcy provides lasting relief without the high fees and risks associated with debt relief programs.

The Simon Fitzgerald LLC Advantage

At Simon Fitzgerald LLC, we prioritize transparency and empowering clients with accurate, actionable information. With over 100 years of experience, we’ve guided thousands of Louisiana residents toward financial freedom through bankruptcy. Our team ensures you fully understand your options and supports you every step of the way.

If you’re weighing debt relief programs against bankruptcy, schedule a free consultation with us to explore your best path forward. Don’t fall victim to scams—choose a proven, legal solution to achieve lasting financial stability.

- Call us at 318-284-5565 (Shreveport/Monroe), 318-526-8551 (Alexandria), or 337-486-3732 (Lafayette/Lake Charles).

- Visit us online: Schedule a Consultation.

FAQS

Why Is Bankruptcy a Better Option Than Debt Consolidation?

- Complete Debt Relief: Bankruptcy eliminates most unsecured debts, offering a fresh financial start, while debt consolidation only reorganizes payments without reducing the overall debt.

- Legal Protections: Bankruptcy provides an automatic stay that halts creditor actions, including lawsuits, wage garnishments, and collection calls, ensuring immediate relief and peace of mind.

- Long-Term Effectiveness: Debt consolidation often fails to resolve underlying financial challenges, leaving you exposed to accumulating interest, missed payments, and potential lawsuits. Bankruptcy, on the other hand, addresses these issues comprehensively, giving you the tools to rebuild your financial future.

Unlike debt consolidation, which merely rearranges payments without addressing the root of financial distress, bankruptcy offers a complete reset. By eliminating or restructuring debts under legal protections, bankruptcy ensures a path to financial stability—free from the risks of creditor lawsuits, garnishments, and escalating fees associated with debt consolidation programs.

How does bankruptcy’s legal protection compare to debt consolidation’s limitations?

Bankruptcy provides the automatic stay, a powerful legal tool that immediately stops lawsuits, wage garnishments, and collection actions. Debt consolidation offers no such protection, leaving you vulnerable to creditor harassment and legal actions even while you make payments.

Can Bankruptcy Protect My Assets?

- Chapter 7 Bankruptcy: Louisiana’s generous exemption laws typically allow you to retain essential assets, such as your home, car, and personal belongings, even while discharging unsecured debts like credit cards and medical bills.

- Chapter 13 Bankruptcy: This reorganization option offers structured repayment plans that safeguard your assets, including your home and vehicle, while providing a pathway to resolve your debts and regain financial stability.

How Does Bankruptcy Affect My Credit, and How Long Does It Stay on My Report?

Concerns about the impact of bankruptcy on credit scores are common, but the reality is that bankruptcy provides a pathway to recovery. While filing for bankruptcy may lower your credit score, the extent of the impact often depends on your financial situation before filing.

- Pre-Filing Credit Health: If your credit score is already low due to missed payments, high credit utilization, or defaults, the decline may be less noticeable. For those with higher credit scores, the initial drop might feel more significant.

- Recovery Timeline: Bankruptcy allows for a fresh start, and many people begin rebuilding their credit within 12-24 months by adopting responsible financial habits. Practices like paying bills on time, maintaining a budget, and using credit wisely can accelerate the recovery process.

Credit Reporting Duration

- Chapter 7 Bankruptcy: Stays on your credit report for 10 years. This duration reflects the significant relief it offers by eliminating most unsecured debts and providing a full financial reset.

- Chapter 13 Bankruptcy: Remains on your credit report for 7 years, as it involves a structured repayment plan to address your debts over time.

The Bankruptcy Advantage

Unlike debt consolidation, which has the potential to prolong financial instability and further damage credit, bankruptcy offers a fresh start. Although it stays on your credit report for several years, lenders often focus on recent financial behavior. With consistent effort and improved habits, you can rebuild your credit and even qualify for loans, credit cards, and mortgages far sooner than expected.

Bankruptcy is not the end of your financial future—it’s the beginning of a stronger, more secure one. By taking this decisive step and committing to smart financial choices, you can regain stability and achieve lasting financial freedom.

How Does Debt Consolidation Affect Your Credit Rating?

Debt consolidation can impact your credit in both positive and negative ways, largely depending on how you manage the process. Understanding these effects can help you make informed decisions about your financial future.

Negative Impacts of Debt Consolidation

- Initial Credit Score Dip: When consolidating debt, opening a new loan or credit account often triggers a hard inquiry on your credit report. This can temporarily lower your credit score.

- Increased Credit Utilization: Closing old credit card accounts or lines of credit after consolidation can raise your credit utilization ratio, which may negatively affect your score.

- Missed Payments: Failure to make timely payments on your consolidated debt could result in late fees, penalty interest rates, and damage to your credit score.

While debt consolidation may simplify payments temporarily, it often fails to resolve the underlying financial issues. Missed or incomplete creditor agreements can still result in lawsuits or collection actions.

Long-Term Outlook

Debt consolidation often gives the illusion of financial improvement while ignoring the root causes of debt. For many clients, it prolongs financial struggles without delivering lasting relief.

While debt consolidation might help in some cases, it’s essential to evaluate whether it addresses the root of your financial challenges. For many individuals, bankruptcy offers a more comprehensive solution by legally eliminating or restructuring debt and providing a clear path to financial recovery.

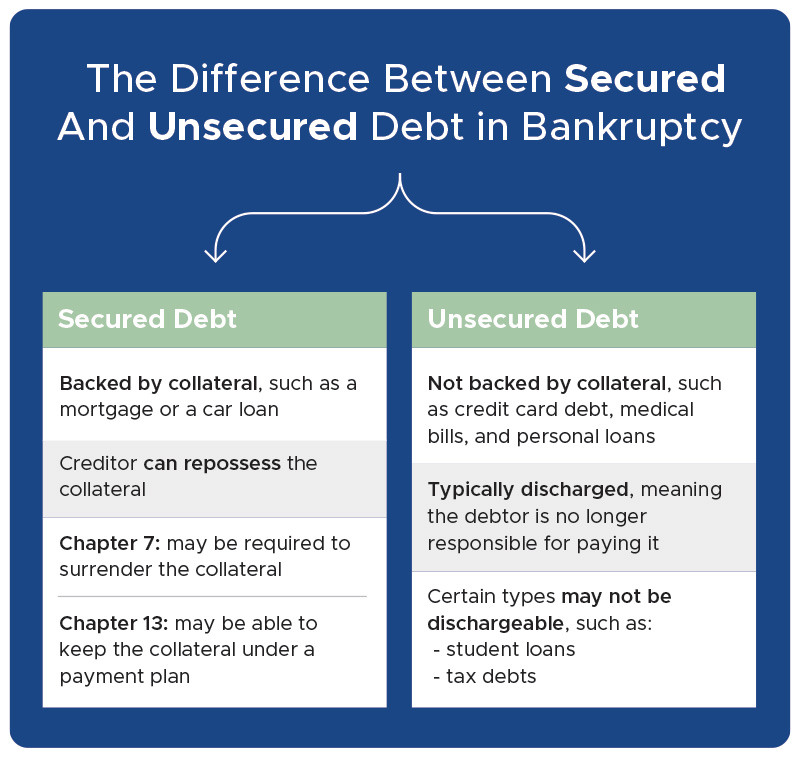

What Types of Debt Can and Cannot Be Erased In Chapter 7 Bankruptcy?

Chapter 7 bankruptcy offers powerful relief by eliminating most unsecured debts while allowing you to keep exempt property. Once discharged, you are no longer legally responsible for repaying these eligible debts, providing a fresh financial start.

Debts That Can Be Erased

Chapter 7 bankruptcy can discharge most types of unsecured debts, including:

- Credit Card Debt: Balances owed on credit cards are typically eliminated.

- Medical Bills: Unpaid medical expenses are commonly discharged.

- Personal Loans: Unsecured personal loans, including payday loans, are usually forgiven.

- Utility Bills: Outstanding balances on utilities can also be included in a discharge.

However, it’s equally important to understand that not all debts can be erased through Chapter 7. Certain financial obligations are considered non-dischargeable under bankruptcy law, meaning you’re still responsible for paying them after your case concludes. Here’s a breakdown of debts that usually can’t be eliminated:

- Federal Student Loans: Federal and private student loan debts are typically excluded from discharge unless you can prove “undue hardship,” which is a difficult standard to meet.

- Child Support and Alimony Obligations: Debt payments for child support and spousal maintenance are considered priority obligations.

- Unpaid Taxes: While some older income tax debts may qualify for discharge under specific conditions (like being several years overdue and properly filed), most recent unpaid taxes remain your responsibility. Payroll taxes and penalties are also non-dischargeable.

- Court Fines and Penalties: If you owe money due to a criminal offense, such as restitution or fines, Chapter 7 won’t erase these debts. Civil penalties, like damages from lawsuits involving fraud or misconduct, typically survive bankruptcy.

- Secured Loans: While Chapter 7 can eliminate your liability for secured debts, such as mortgages or car loans, creditors can still reclaim the property tied to these debts if you don’t make consistent payments.

Understanding Exemptions and Protections

Louisiana’s generous exemption laws often allow you to keep essential assets, such as your primary home, vehicle, household goods, and retirement accounts. These protections help ensure that filing for Chapter 7 bankruptcy doesn’t mean losing everything you own.

Chapter 7 bankruptcy is an effective tool for wiping out overwhelming unsecured debt, but it’s essential to understand which obligations will remain. With guidance from an experienced bankruptcy attorney, you can make informed decisions about how to achieve financial freedom while protecting your most important assets.

Questions? Speak to a Louisiana Bankruptcy Attorney Today

Take Control of Your Financial Future

Avoid being persuaded by debt consolidation companies that bankruptcy is the final option. At Simon Fitzgerald LLC, we’ve helped thousands of Louisiana residents achieve lasting financial freedom through bankruptcy. Our experienced attorneys provide honest, straightforward advice to empower you with the knowledge you need to make the best decision for your future.

Why Choose Simon Fitzgerald LLC?

- Expertise You Can Trust: With over 100 years of experience, we specialize in guiding individuals and families through the bankruptcy process.

- Clear and Compassionate Guidance: We’re here to educate you about your options, not to pressure you into a decision.

- Tailored Solutions: We focus on your unique financial situation to help you achieve a fresh start.

Schedule Your Free Consultation

We’re committed to making the process as stress-free as possible. Whether you’re considering bankruptcy or evaluating alternatives like debt consolidation, we’ll provide the facts so you can decide on the best course of action.

Call Us:

Schedule Online: Book Your Free Consultation.

What to Expect During Your Free Consultation

- A No-Cost, No-Obligation Discussion: We’ll review your financial situation in detail and outline your available options.

- Answers to Your Questions: Learn the facts about bankruptcy and debt consolidation so you can make an informed decision.

- Personalized Solutions: We’ll help you understand which debt relief option best aligns with your financial goals.

Don’t let overwhelming debt dictate your future. Contact Simon Fitzgerald LLC today and take the first step toward financial freedom.